What Is The Name Of The Tax Paid On All Goods And Services In Switzerland?

Rate this article

based on two reviews.

When starting a concern in Switzerland , foreign entrepreneurs should be interested in finding out information about the taxes applied at a national level. Switzerland levies direct or indirect taxes . The direct taxes are applied on income and wealth, while the indirect taxes are applied to appurtenances and services and it also includes the Value Added Taxation (VAT) . Due to Switzerland's political organization the tax system is organised on the following: the confederate revenue enhancement system , the cantonal taxation system and the municipal tax system , each i applied individually. Switzerland has 26 cantons and 2600 municipalities based on the Federal Constitution and cantonal regulations. Our team of lawyers in Switzerland can offering more information on the taxes imposed to both natural persons and legal entities.

Types of taxes in Switzerland

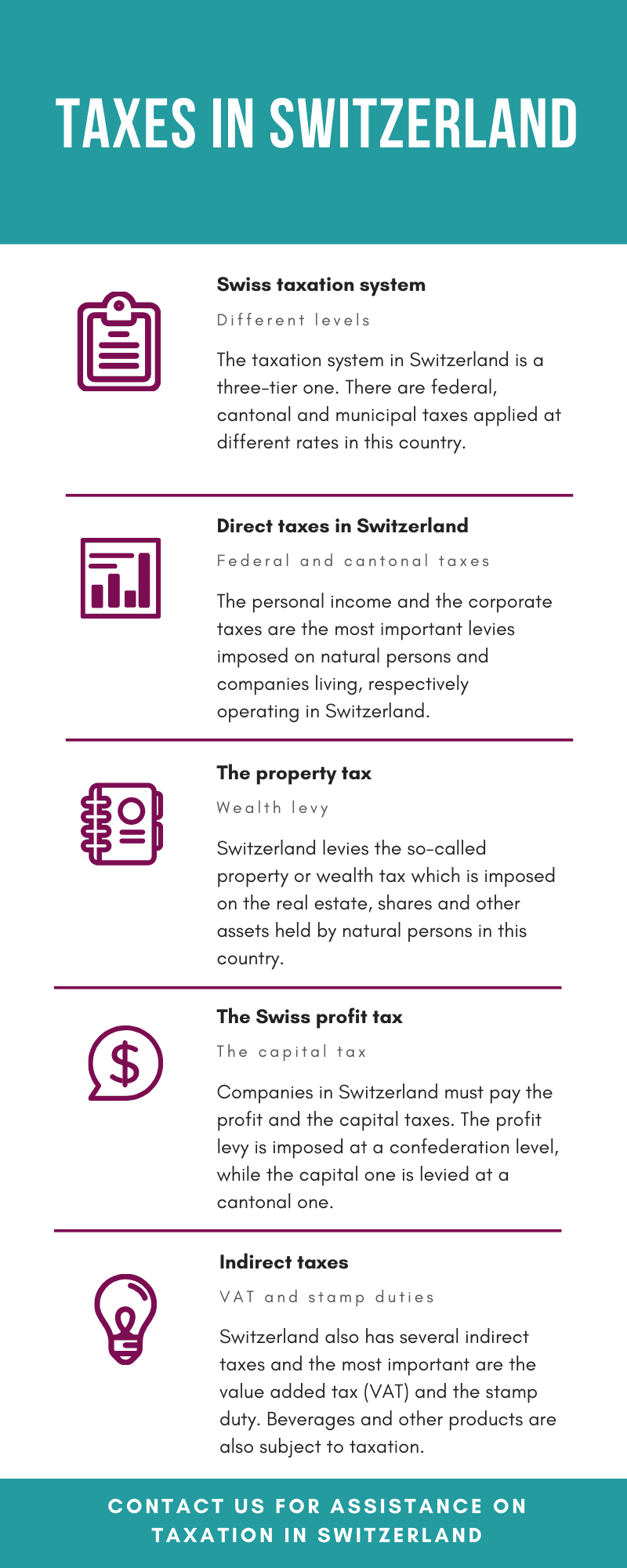

Taxation in Switzerland is based on a iii-tier system levied at federal, cantonal and municipal levels, however, merely like in other European jurisdictions, both natural persons and companies are bailiwick to direct and indirect levies.

Here are the main taxes that demand to be considered when paying them in Switzerland:

-

the income tax which levied on natural persons on a progressive basis;

-

the corporate tax which is levied on all iii levels (federal, cantonal, communal);

-

the value added taxation which is the most important indirect levy in Switzerland;

-

withholding taxes which are imposed on various incomes, such as dividends, interests, royalties.

When considering moving or starting a business in Switzerland, virtually foreign citizens and investors cull the all-time canton based on the taxes levied, as these brand the departure between the college and lower tax rates. Our police force firm in Switzerland can offer more than data on how taxes are calculated in this country.

The federal and cantonal taxes in Switzerland

The direct taxes are bachelor for natural persons and are applied for income and wealth. Other taxes include the corporate taxes on profit and capital letter.

The Federal taxes are: the Value Added Taxation (VAT), the withholding revenue enhancement, stamp duties, edge and other taxes.

Directly Taxes in Switzerland

The income taxation in Switzerland

The income tax is levied by the Confederation and by the cantons and it can be progressive or proportional on the income of a natural person; it is imposed equally a payroll tax for strange workers without a residence permit and as a withholding taxation on transient persons.

Not-working foreigners may choose to pay a "lump-sum revenue enhancement" which is lower than the regular income revenue enhancement and information technology varies from canton to canton, its lowest value existence the quintuple of the rent paid by taxpayer.

It is of import to know that the income below CHF 14,500 is exempt of the income tax. At a federal level, the income revenue enhancement is imposed on a progressive basis, which ranges from 0.77% to eleven.5% of the total income of a natural person. Natural persons interested in the taxation system bachelor in Switzerland should also know that the personal revenue enhancementis imposed on a different organization, in accordance with the legal statute of the individual (single or married).

The post-obit rates must be considered when it comes to the taxation of natural persons in Switzerland:

-

the first fourteen,500 CHF are exempt from taxation in Switzerland;

-

for unmarried taxpayers the everyman income tax rate is established at 0.77%;

-

for married taxpayers, the lowest tax charge per unit is 1% for an income of 28,300 CHF;

-

the highest rates are 13.twenty% in for unmarried taxpayers and 13% for married couples.

Individuals living in Switzerland must likewise consider the cantonal taxes they demand to pay. Likewise, foreign citizens and companies must register with the Federal Department of Finance.

The primary taxes to exist paid in Switzerland are likewise presented in the infographic below:

The wealth or property tax in Switzerland

Information technology is set at 0.3 to 0.five per cent on the net worth of natural persons and it is levied on the value of all their avails (real estate backdrop, shares or funds). This taxation is set at cantonal and communal level. The tax base is different in the case of married persons.

The corporate taxes in Switzerland

Corporate taxes are assail profit and capital. Due to taxation of both corporation and its owners or shareholders, the corporate tax is decumbent to double tax. All legal persons comply with the taxation of capital and profit, except for charitable organizations. The corporate tax rate applicable at a national level is established at eight.5%. Depending on the canton, the corporate tax rate tin vary, as the Swiss authorities impose a cantonal revenue enhancement charge per unitas well. As a full general dominion, the overall corporate tax rate varies betwixt 12% and 24%, depending on the region in which the company was incorporated.

The profit tax in Switzerland

The profit revenue enhancement is established at Confederation level and it is proportional or progressive at a flat charge per unit of viii.5%, or at canton level which varies. It is based on the net profit equally accounted for in the corporate income statement and adapted for tax purposes. There are also provisions that limit double taxation according to tax treaties, such as "participation exemption" for companies that own 20% or more of the shares of other companies, a ''holding privilege" for companies that are exempt from cantonal corporate profit tax, and "domicile privilege" for companies based exterior Switzerland and but administered in Switzerland.

The capital tax in Switzerland

It is a proportional tax levied by cantons at varying rates on the ownership equity of companies and works as if companies are taxed for the liabilities that function as disinterestedness. These debts cannot be deducted for purposes on the profit tax and are subject to the federal withholding taxation. Our law firm in Switzerland will be at your disposal with more information in this matter.

Investors should know that companies operating in Switzerland are required to file for tax returns on the capital tax on a yearly basis. The procedure is handled at a cantonal level.

Federal Taxation in Switzerland

The federal taxes on goods and services are the post-obit:

- the VAT tax

- stamp duties;

- the tobacco tax;

- the beer tax;

- the tax on distilled spirits;

- the mineral oil taxation;

- the motor vehicle taxation;

- the motorway vignette;

- the distance-related heavy vehicle fee;

- customs duties.

Cantonal and municipal taxes on goods and services

Cantonal and municipal taxes on goods and services include:

- taxes on motor vehicles;

- dog taxes;

- entertainment tax;

- stamp and registration duties;

- water duty;

- lottery tax;

- visitor'south tax.

Value added tax

The VAT - Value Added Taxation in Switzerland is i of the Confederation's main sources of income. It is set at 8% on most commercial exchanges of goods and services, except for food, drugs, books and newspapers, that are subject area to 2.5 % VAT. Medical, educational and cultural services are not subject to VAT registration in Switzerland, and so are the goods and services provided away. The standard VAT rate of 8%was established in Switzerland in 2011. Every bit mentioned to a higher place, the Swiss authorities besides provide lower VAT rates and in the instance of companies operating in the accommodation industry, it is important to know that the VAT charge per unit is imposed at the rate of iii.8%.

Companies opened in Switzerland are required to file the appropriate VAT to the local government and, at the same time, they are also required to keep the books of records for a period of 10 years.

The VAT rates imposed in Switzerland are much lower that the VAT rates bachelor across the European Union (European union) due to the fact that the state is not a fellow member of the Community. Thus, the local regime are allowed to impose the rate which is considered suitable for the current needs of the Confederation.

Federal withholding tax in Switzerland

The federal withholding tax is levied at 35% on dividend payments, interest on depository financial institution loans and bonds, liquidation procedures, lottery prizes, life insurance payments and private pension funds.

Debtors of such payments have to pay the tax, as for creditors it is just a way of making sure the profit revenue enhancement is being paid, but the creditor can deduct the amount or ask for a refund. If a revenue enhancement treaty exists, foreign creditors tin too benefit of the refund.

Stamp duties in Switzerland

Stamp duties are taxes in Switzerland levied on commercial transactions. These are the result taxation and the transfer tax. The first i is practical to shares and bonds while the 2d one to trading certain securities by qualified traders such as stockbrokers and big companies. The transfer tax varies from 0.15 to 0.3 per cent depending on the provenience of the securities, to be exact, if they are Swiss or strange. Likewise an insurance premiums tax of 5 or 2.5 per cent is levied on certain insurance premiums. The contributions to the equity of a company in Switzerland are imposed with a stamp duty of one%.

Foreign investors interested in mergers and acquisitionsmust also know that such procedures, including the reorganisation of the company, isexempt of the stamp duty.

At the same time, the re-domiciliation of a foreign company in Switzerland is also exempt of the stamp duty.

Border duties and other taxes in Switzerland

The Confederation has the power given by constitution to levy tariffs that are used every bit an instrument of trade policy. Also the import or manufacture of alcoholic beverages, tobacco, automobiles and mineral oil or gambling establishments are subject to federal taxes. Also, citizens that do not attend military service have to pay a tax in return.

Other than the taxes in Switzerlandhigher up, the cantons are complimentary to introduce other taxes such equally an inheritance tax, the gift revenue enhancement, church tax, a tax on the profit from selling a house.

Taxation residency for individuals in Switzerland

In gild to decide the taxes that need to be paid as a natural person in Switzerland, specific rules must exist respected. These refer mainly to the residency of the taxpayer which has a straight influence on the levies and amount of money to be taxed in this state.

An individual is considered a tax resident in Switzerland if he or she has a place to stay hither. Besides, permanent residents are considered taxation residents in Switzerland, therefore they will exist taxed on their worldwide income.

In the example of foreign citizens, these are considered revenue enhancement residents in Switzerland if they alive and earn money for a minimum catamenia of 30 days in a calendar year. Those living in Switzerland for at least 90 days without gaining money here are also accounted as tax residents hither. The exception to these rules applies to students and persons coming here for various medical treatments.

Government officials and individuals working for various organizations are subject area to special criteria and are liable to pay the income tax in Switzerland on the money earned here. They also fall nether specific regulations imposed in Switzerland' double tax treaties.

Strange citizens not falling under any of the categories mentioned above merely all the same earning coin here will be taxed on the income obtained here by filing specific revenue enhancement forms.

Our Swiss lawyers can offer more information on how to obtain residency and citizenship here.

Taxation residency for companies in Switzerland

Liability based on tax residency does not apply to individuals only, as companies must also meet certain criteria in club to pay the corporate tax on their worldwide profits here.

A company is considered tax resident in Switzerland if it has a registered office or identify of management in this land. Notwithstanding, non-resident companies tin can also bear various operations in Switzerland. Tax residency is important in lodge to establish the liability related to the taxes paid in this country.

In most cases, the residence of a visitor is based on the country of registration. The post-obit situations can exist encountered:

-

a company can be registered in Switzerland and automatically exist considered a revenue enhancement resident here;

-

a company tin can be registered abroad and sell or provide goods, respectively services in Switzerland without having an established presence here;

-

a company can exist registered abroad but have a place of management in Switzerland, thus obtain the status of revenue enhancement resident.

The latter case applies to branch offices and subsidiaries of foreign companies operating in Switzerland through permanent establishments.

An of import attribute to consider about the taxation of companies in Switzerland refers to the shareholders and managers. In most cases, where a manager or shareholder is a Swiss resident, the company can be deemed equally a domestic company.

Our lawyers in Switzerland can offer more data on how fiscal dwelling is established in the case of companies. You tin can likewise rely on us for help in registering a company here.

What Is The Name Of The Tax Paid On All Goods And Services In Switzerland?,

Source: https://www.lawyersswitzerland.com/taxation-in-switzerland

Posted by: boydflid1954.blogspot.com

0 Response to "What Is The Name Of The Tax Paid On All Goods And Services In Switzerland?"

Post a Comment